Unite members at Hull & East Riding Citizens Advice are beginning strike action over a pay dispute with their employer.

For more than 20 years, our members have had an agreement with Hull CAB to give pay increases in line with the local authority NJC pay scale. For over 10 years, this has meant workers receiving zero or below-inflation pay increases.

In 2022/23, the NJC award was larger, and faced with this the employer will not pay up and has broken the long-term deal with Unite members.

Hull CAB has healthy reserves which have increased from £100k to £1.1 million over the last 10 years, and it has an annual income of £3.4 million. It can easily afford to meet our members’ reasonable demands.

Join us at the first day of strike action at 9am this Monday 31 July outside the Wilson Centre, Alfred Gelder Street, Hull, HU1 2AG

If you’re in area, please try and make it along to the picket.

The pandemic, soaring inflation and energy costs, stagnating wages and years of attacks on social security have created the worst household debt crisis in living memory.

The Money & Pensions Service funds debt advice with an annual levy on businesses. But this is only paid by consumer credit and mortgage lenders, and other businesses which create or profit from household debt, such as energy, water, telecoms and bailiff firms do not have to pay it.

Yet many of these firms are making obscene profits. In February alone:

British Gas parent company Centrica announced its annual profits had trebled to £3.3bn

Energy company EDF announced annual profits of £1.1bn

The big 4 UK banks announced £19.8bn profit in a 9-month period

Politicians have a choice to make. The government must urgently increase the debt advice levy. There is precedent for this when the levy was increased in 2020 in anticipation of higher demand during the pandemic, but the demand for debt advice now is far higher than it was three years ago.

The government must also extend the levy to all businesses which contribute to household debt problems. Corporate profiteers like the big energy firms cannot be allowed to take billions out of our economy without paying their fair share towards fixing a debt crisis they helped to create.

Unite’s national officer for the Community, Youth Workers and Not-for-Profit sector, Alan Scott – himself a former debt adviser – has written to the chancellor Jeremy Hunt MP to set out these demands.

Our day of action

On Monday 13 March, Unite for a Workers’ Economy organised a historic first day of action in London in protest at the underfunding of vital debt advice services.

Demonstrations were held outside the three government departments which control debt advice funding – the Department for Work & Pensions, HM Treasury and the Money & Pensions Service.

Frontline workers from Unite Debt Advice Network travelled from as far as Cornwall to stand up for better pay and conditions, and a better service for their clients. And Unite Community members from across the London and Eastern region, many living on low incomes and affected severely by the cost of living crisis, joined the demos.

At the same time, supporters around the country bombarded the social media accounts of the three government departments with our Save Debt Advice message.

We handed in copies of a petition supporting our demands, and signed by nearly 2,000 Unite members and debt advice workers. A slate of debt advice experts addressed the demos, including:

Tanis Belsham-Wray, chair of Unite West Yorkshire & Humber Community, Youth Workers and Not-for-Profit branch

Alan Scott, Unite national officer for the Community, Youth Workers and Not-for-Profit sector

They spelled out exactly why debt advice is essential, and why secure jobs, decent pay and manageable workloads are critical to keep services running – and that means an emergency injection of funding.

This day of action marks an escalation in the campaign to Save Debt Advice, and if our demands on the chancellor are ignored, action will continue.

Debt advice services have never been more vital, and across the sector we’re hearing of unprecedented demand. Client numbers are soaring and cases are becoming increasingly complex and time-consuming.

Yet we’re also seeing funding cuts and adviser jobs at risk:

Money & Pensions Service (MaPS) funding for community-based services has been cut by over 20% in real terms compared to before the pandemic.

We need more debt advisers, and that means more funding. It’s time to step up our campaign.

What is Unite calling for?

MaPS funds debt advice with an annual levy on businesses. But this is only paid by consumer credit and mortgage lenders. Other businesses which also create or profit from household debt, such as energy, water and telecoms firms do not have to pay it.

Many of these firms are making huge profits – in February alone:

British Gas parent company Centrica announced its annual profits had trebled to £3.3bn

Energy company EDF announced annual profits of £1.1bn

The big 4 UK banks announced almost £20bn profits in a 9-month period

We are calling on government to increase and expand the debt advice levy so all businesses which profit from household debt pay towards fixing the debt problems they helped to create. This extra funding is vital if we are going to cope with extra demand and ensure debt advisers have decent pay, manageable workloads and job security.

Unite is writing to HM Treasury this week to set out our demands, but we need to take more action to ensure our voice are heard.

Come to our London day of action – Monday 13th March

Join Unite activists demonstrating on Monday 13th March at the three government departments which are responsible for administering debt advice funding.

11.00 – 11.45 –Demo at Department for Work & Pensions (DWP), Caxton House, Tothill Street, SW1H 9NA (nearest tube St James Park)

13.15 – 14.00 – Demo at Money & Pensions Service (MaPS), 120 Holborn, EC1N 2TD (nearest tube Chancery Lane)

This is the first time these organisations have seen a demo about this issue, so we need as many people there as possible to ensure they can’t ignore us.

Let us know if you’re coming here or at our Facebook event page here

Join our social media storm – Monday 13th March

Supporters around the country can join in online by sending messages to the three government agencies between 11.00 and 14.00 on March 13th.

There’s full instructions and a downloadable poster here

Debt advice has never been more important as millions of households struggle, yet funding cuts threaten access to this service and our members’ jobs. Money is there to increase funding, but government refuses to make businesses pay to fix the problem they helped to create.

Funding from the Money & Pensions Service (MaPS) for the community-based debt advice services offered by Citizens Advice, Law Centres and others has been cut by over 20% in real terms compared to before the pandemic.

Funding of national services is in disarray, and Unite members at StepChange Debt Charity in Leeds are facing an estimated 200 job losses as a result.

All this at a time when demand for debt advice is at a record high, and getting worse.

MaPS funding comes from an annual levy on consumer credit and mortgage lenders. We are calling for this levy to be increased, and extended so that all organisations which create or profit from household debt pay towards debt advice.

For example water, energy, telecoms and bailiff firms currently contribute nothing to the levy. Many companies in these sectors are making higher profits now than before the pandemic, so can easily pay towards fixing the debt mess they have contributed to.

‘Save debt advice’ day of action – 13th March

Unite for a Workers’ Economy is organising a ‘Save Debt Advice’ day of action in London with demonstrations at three key government departments on Monday 13th March – full details here

We are calling on the government and MaPS to increase debt advice funding by extending the levy, to cope with the huge spike in demand following the pandemic and cost of living crisis.

Here’s how you can join our day of action

1. Sign our petition, and ask your friends and colleagues to sign it too

2. Come along to our day of action in London – let us know if you’re coming here. If you can’t come in person, join in our online supporting action – more details of this soon

3. If your Unite branch has online meetings, ask us along to talk about the day of action and the issues involved. Depending on location, we may be able to attend in-person meetings too

On 4th October 2022 the Money and Pensions Service (MaPS) announced the final tranche of contract awards in respect of its rather long-winded and troublesome procurement of debt advice services. The latest announcement encompassed its 3 (three!) national debt advice contracts, a business debtline and 2 ‘administration of debt relief orders’ hubs. This followed the announcement on 29th September 2022 of 26-month grants to fund community-based debt advice services. (Read the full MaPS’ announcement here.)

MaPS stated that:

Once the new contracts and the grants are live, MaPS will be investing £76m per year into debt advice services. This is an 80% increase compared with 2019.

I’m old enough to remember when MaPS announced the £77m funding pot back in May 2021, so what happened to that £1million?

Based on the stated 80% increase, simple maths means that pre-pandemic funding of debt advice in England was £42.2m per annum right?

***

Let’s go back to December 2017 and the Money Advice Service (MaPS’ predecessor). In its publication, ‘A strategic approach to debt advice commissioning 2018–2023’, MAS stated that ‘around £45m from the FCA levy’ was used to fund ‘around 65%’ of all face-to-face debt adviceand ‘significant amounts’ of telephone and digital advice across the UK. It further stated that ‘at least £150m a year goes towards funding free-to-client debt advice’, which MAS described as funding from local authorities, trusts, devolved governments, ‘FairShare’ (£50m a year based on £450m being repaid via debt management plans (DMPs)) and debtors themselves via commercial-sector DMPs.

…hard data are hard to come by, but a reasonable estimate of the total cost of debt advice provided in 2016/17 is in the region of £200m.

When looking at MAS’ estimate of funding levels — either MAS have underestimated, or Mr Wyman has overestimated. Regardless of actual data or the cited ‘limited amount of hard evidence’, it came as no surprise that Mr Wyman’s recommendations included ways to:

improve the efficiency of supply by reducing duplication and encouraging wherever possible greater use of technology and the lowest cost delivery channel.

***

The Financial Conduct Authority (FCA) is the organisation responsible for collecting levies to provide MAS/MaPS with money to fund debt advice and, luckily, has less hazy figures for us to peruse — in fact, we can track them annually.

2016/17 (9.2) — The total budget for MAS debt advice (UK) in 2016/17 is £45m

2017/18 (9.15)— The total budget for MAS debt advice (UK) in 2017/18 is £48m

2018/19 (8.13 )— The total budget for MAS debt advice (UK) in 2018/19 is £56.3m (includes additional £3m to set up MaPS)

2019/20 (7.8) — The total budget for delivering the MaPS debt advice function (England only) for 2019/20 is £53.3m (This, you might argue, is the pre-pandemic figure which should be used in regard to the recent funding announcement…read on.)

2020/21 (9.5 & 9.10) — The proposed budget for delivering the MaPS debt advice function in England is £64.6m, however the final budget is £63.2m. Now, this is the figure I would use; the ‘business as usual’ pot of money for debt advice.

An additional £37.8m of funding was then made available (£20.6 million from Government, £14.2 million through a one-off increase to the debt advice levy and a further £3 million contribution from MaPS.) The total budget for delivering the MaPS debt advice function (England only) for 2020/21 is £101m.

2021/22 (7.8) — The proposed budget for delivering the MaPS debt advice function is £94.6m, however the final budget is £85.3m.

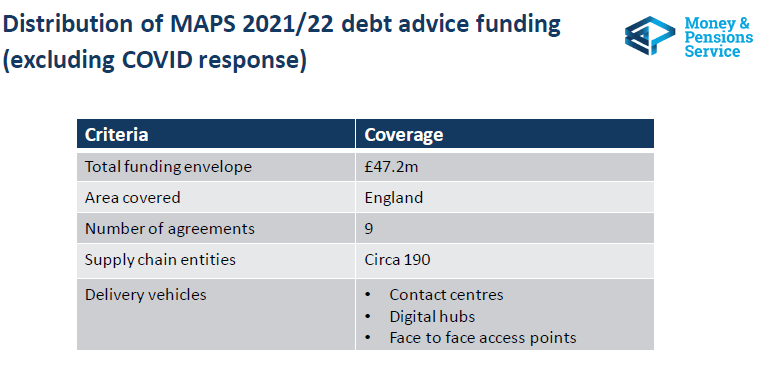

It is interesting to note that the ‘total funding envelope’ cited by MaPS in their early commissioning slides from May 2021 is £47.2m. A difference of £38.2m to the FCA levy and a serious cut to the 2020/21 ‘business as usual’ funding of £63.2m.

From ‘Commissioning Debt Advice in England — Market Engagement Webinar’ slide deck

2022/23 (7.3) — The proposed budget for delivering the MaPS debt advice function is £91.4m, however the final budget is £80.7m

Blue represents ‘business as usual’ funding and orange represents ‘increased debt advice capacity’ (IDAC funding during the outbreak of Covid

Now let’s turn to the MaPS Corporate Plan for 2021/22 and try to put the above into context. The below pie chart demonstrates the total budget for MaPS including its pensions and money advice functions.

MaPS 2021/22 Corporate Plan indicates a budget of £94.6million for debt advice

MaPS provides a figure of £94.6m for provision of debt advice. However, thanks to the FCA publications above, we know it didn’t receive £94.6m, but £85.3m. MaPS also didn’t receive anything like the total of £157.4m published in its Corporate Plan, of which £147.6m was ring-fenced for ‘resource spending’. The actual figure confirmed by the FCA is £127.5m; they said:

We have adjusted these to reflect underspends, notified to us by the DWP, on the amounts collected under last year’s money guidance, pensions guidance and debt advice levies.

Let’s go back to that 80% increase, cited at the beginning. The 2020/21 debt advice funding pot was £63.2m – the increase to £76m in 2023/24 is 20% at best.

If we err on the side of generosity and plum for the 2019/20 figure of £53.3m then the £76m represents an increase of 42%. It’s better, but it’s a long way off 80%.

Even we go along with the £47.2m funding ‘envelope’, it’s a 60% increase. So where on earth does 80% come from?

Current funding of community advice until the end of January 2023 is £33.6m — this leaves £47.1m funding remote advice (contact centres). We can say with some confidence that the community grants for February 2023 (£30m) represent a definite 10% cut to community funding.

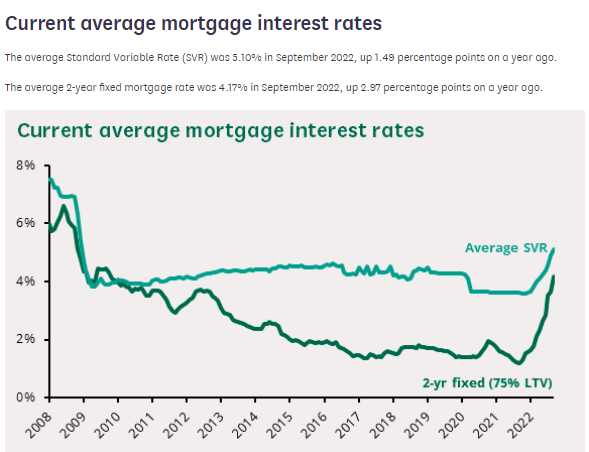

Some would argue (and I’m one of them) that the cost of living crisis, the highest rates of inflation for 40 years, personal indebtedness soaring and mortgage rates looking like this:

…require the same additional funding to debt advice that the pandemic warranted, if not more. This would help community organisations balance their own tightened budgets, recruit the staff they need to meet increased demand, continue the training of staff taken on in 2020 and, maybe, even give their existing staff a decent payrise.

***

Finally, there remains the problem of the apportionment of the budget in favour of remote advice. Mr Wyman (p19, point 33) concluded it was cheaper to give debt advice ‘online’ (£9 — per what?? Hour? Contact?), or by telephone (£70 per ??) than in person: a whopping £160 per….something. Well, of course it is! Because you are doing so much less for the people who need the help. And if each person who needed that in depth advice, comes away from these remote experiences with a 6-inch thick info-pack on every debt solution known to mankind, the risk is that the advice won’t help them at all — and we’ll never know.

Unfortunately, MaPS were convinced by the cheaper = more = value for money argument, and the debt advice ‘sector’ is infested with impressive but utterly meaningless statistics. 500 calls ‘dealt with’ is not the same as 500 people achieving a useful outcome. 500 people advised to claim a benefit is not the same as 500 people actually claiming and receiving that benefit.

I’m very wary of organisations who suggest that they ‘empower’ clients by sharing information from a website/benefit calculator/budgeting tool, when what the client needs is a expert professional to sit with them, read their letters, give them time, advise them and, yes, empower them with knowledge, and a plan. True empowerment is a thing you can witness in advice.

Professional advisers don’t foist useless in-depth advice on people who don’t need it either. We are completely able to offer light touch advice or signpost information if that’s what the client needs.

We can also do remote advice — we use telephones and webchat and video-conferencing. Some of us even use WhatsApp!

***

This whole procurement exercise has been flawed from the start. We Are Debt Advisers wanted the whole thing scrapped, with proper consultation and a better understanding by MaPS of what debt advice is before it gave £46m of precious funding to remote services, especially when one of the remote service providers is a commercial, profit-making entity with a not exactly glowing reputation. That opportunity is now gone, but it is to be hoped that MaPS’ promise to engage with frontline advisers is a sincere one, and that we can yet turn this ship around.

In 2021, MaPS launched a recommissioning process which would have seen cuts of 50% or more in community-based face-to-face debt advice, with funding moving towards telephone and online services. These work for some people, but are simply inaccessible for many people our members support.

Following a campaign led by UDAN and We Are Debt Advisers (WADA), the recommissioning process was halted, saving hundreds of debt advice jobs. As a short-term measure, MaPS extended the existing funding for community-based services. This had been due to end on 31 March 2022, but a further 10 months of funding was announced, securing jobs and services until 31 January 2023.

This was good news for our members, many of whom were preparing for redundancy. As WADA reported in December 2021, many debt advisers were expecting to lose their jobs and seeking other employment. Sadly, many experienced advisers left the sector at this time, and recruitment into the resulting fixed-term vacancies became very difficult.

MaPS announced this would be a ‘test and learn’ period, where future services would be shaped by engagement with debt advice providers and advisers. There have been some meetings since, including between UDAN and MaPS to discuss what our members and clients need.

Extension of funding

On 29 September, MaPS announced the end date for the current funding of community-based services is to be extended from 31 January 2023 to 31 March 2025.

This means our members working in MaPS-funded services have job security for a further two years.

This funding was a crucial source of income for many small services, many of which do brilliant work, rooted in their local communities. Some services had been clear in 2021 that ending this funding would mean their entire service would be at risk. This week’s announcement secures these services for an extra two years.

As the cost of living crisis deepens, these services will be needed more than ever. The extended funding is also great news for people in debt crisis, who will continue to have access to debt advice experts in their communities.

What’s next?

We welcome the extended funding for all the reasons above, but there is still much work to be done. We are pleased to see that MaPS has committed to proper consultation through a new ‘Debt Adviser Panel’. How this panel is set up and operated will be of key importance – it must be the genuine voice of frontline debt advisers. Critically, MaPS must act on the findings to make permanent improvements.

We are pleased to hear that MaPS is moving away from numeric targets to a focus on outcomes – one of UDAN’s initial demands.

With medium-term job security assured, we now need to see action on:

Improved pay in debt advice workplaces, including a clear progression path from trainee to experienced adviser with accompanying pay increases

Long-term security for jobs and funding, not wasteful and destabilising competitive tender processes every few years

Sufficient staffing to meet demand, to relieve our members of unmanageable workloads and unpaid overtime

Better practical support for debt advisers, such as free access to credit reports and both translation and interpreting services

MaPS is the sector’s largest funder, and therefore has a central role in setting pay and conditions. These improvements for MaPS-funded advisers would encourage other providers to improve their pay and conditions.

UDAN has now launched a comprehensive survey of pay and working hours in debt advice workplaces.

This builds on the findings in the IMA’s 2019 Salaries in the debt advice sector report, and we are looking in more detail at working hours, other remuneration, how pay awards are decided, and inequalities in pay.

This survey is aimed at everyone working in a free-to-client debt advice service in the UK, and we want to hear from union members and non-members to get the fullest possible picture.

The survey is anonymous and does not ask for any information which could identify you or your employer.

Unite Debt Advice Network (UDAN) conducted a short survey this week to find out if debt advisers are expecting a pay rise this year, and if this will meet inflation. We asked 40 debt advisers and found that:

32.5% had not received, and were not expecting to receive, a pay rise at all this year

57.5% were to receive a pay rise this year

Of those receiving a pay rise, the mean was 3.16% (min 1.5%, max 7%, median 3%)

The mean pay increase this year across all the whole sample was 2.02% (median 2%)

This falls far short of current inflation (7.9% CPIH or 13.4% RPI in May 2022[1])

This represents a substantial real-terms pay cut for our members at a time when pressure on our services is growing rapidly.

UDAN will be conducting further research into debt adviser pay, and a detailed survey of members and non-members will be sent out in the coming weeks.