As we approach MaPS Talk Money week, Amy Taylor, chair of Greater Manchester Money Advice Group and We Are Debt Advisers talks money…

On 4th October 2022 the Money and Pensions Service (MaPS) announced the final tranche of contract awards in respect of its rather long-winded and troublesome procurement of debt advice services. The latest announcement encompassed its 3 (three!) national debt advice contracts, a business debtline and 2 ‘administration of debt relief orders’ hubs. This followed the announcement on 29th September 2022 of 26-month grants to fund community-based debt advice services. (Read the full MaPS’ announcement here.)

MaPS stated that:

Once the new contracts and the grants are live, MaPS will be investing £76m per year into debt advice services. This is an 80% increase compared with 2019.

I’m old enough to remember when MaPS announced the £77m funding pot back in May 2021, so what happened to that £1million?

Based on the stated 80% increase, simple maths means that pre-pandemic funding of debt advice in England was £42.2m per annum right?

***

Let’s go back to December 2017 and the Money Advice Service (MaPS’ predecessor). In its publication, ‘A strategic approach to debt advice commissioning 2018–2023’, MAS stated that ‘around £45m from the FCA levy’ was used to fund ‘around 65%’ of all face-to-face debt advice and ‘significant amounts’ of telephone and digital advice across the UK. It further stated that ‘at least £150m a year goes towards funding free-to-client debt advice’, which MAS described as funding from local authorities, trusts, devolved governments, ‘FairShare’ (£50m a year based on £450m being repaid via debt management plans (DMPs)) and debtors themselves via commercial-sector DMPs.

It’s all guesswork, and in his Independent Review of the Funding of Debt Advice [in the UK], published in 2019, Peter Wyman suggests:

…hard data are hard to come by, but a reasonable estimate of the total cost of debt advice provided in 2016/17 is in the region of £200m.

When looking at MAS’ estimate of funding levels — either MAS have underestimated, or Mr Wyman has overestimated. Regardless of actual data or the cited ‘limited amount of hard evidence’, it came as no surprise that Mr Wyman’s recommendations included ways to:

improve the efficiency of supply by reducing duplication and encouraging wherever possible greater use of technology and the lowest cost delivery channel.

***

The Financial Conduct Authority (FCA) is the organisation responsible for collecting levies to provide MAS/MaPS with money to fund debt advice and, luckily, has less hazy figures for us to peruse — in fact, we can track them annually.

- 2016/17 (9.2) — The total budget for MAS debt advice (UK) in 2016/17 is £45m

- 2017/18 (9.15)— The total budget for MAS debt advice (UK) in 2017/18 is £48m

- 2018/19 (8.13 )— The total budget for MAS debt advice (UK) in 2018/19 is £56.3m (includes additional £3m to set up MaPS)

- 2019/20 (7.8) — The total budget for delivering the MaPS debt advice function (England only) for 2019/20 is £53.3m (This, you might argue, is the pre-pandemic figure which should be used in regard to the recent funding announcement…read on.)

- 2020/21 (9.5 & 9.10) — The proposed budget for delivering the MaPS debt advice function in England is £64.6m, however the final budget is £63.2m. Now, this is the figure I would use; the ‘business as usual’ pot of money for debt advice.

- An additional £37.8m of funding was then made available (£20.6 million from Government, £14.2 million through a one-off increase to the debt advice levy and a further £3 million contribution from MaPS.) The total budget for delivering the MaPS debt advice function (England only) for 2020/21 is £101m.

- 2021/22 (7.8) — The proposed budget for delivering the MaPS debt advice function is £94.6m, however the final budget is £85.3m.

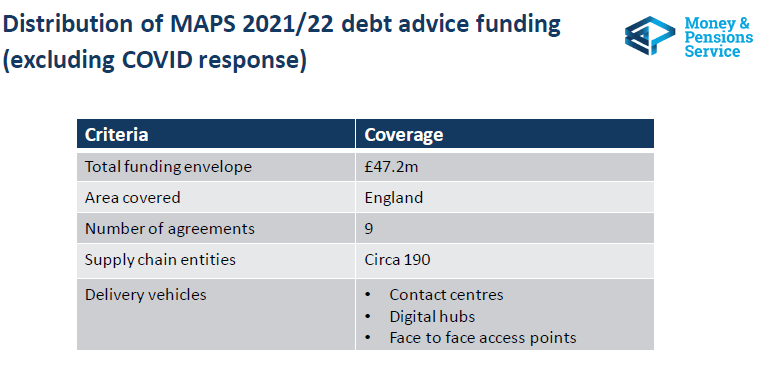

- It is interesting to note that the ‘total funding envelope’ cited by MaPS in their early commissioning slides from May 2021 is £47.2m. A difference of £38.2m to the FCA levy and a serious cut to the 2020/21 ‘business as usual’ funding of £63.2m.

- 2022/23 (7.3) — The proposed budget for delivering the MaPS debt advice function is £91.4m, however the final budget is £80.7m

Now let’s turn to the MaPS Corporate Plan for 2021/22 and try to put the above into context. The below pie chart demonstrates the total budget for MaPS including its pensions and money advice functions.

MaPS provides a figure of £94.6m for provision of debt advice. However, thanks to the FCA publications above, we know it didn’t receive £94.6m, but £85.3m. MaPS also didn’t receive anything like the total of £157.4m published in its Corporate Plan, of which £147.6m was ring-fenced for ‘resource spending’. The actual figure confirmed by the FCA is £127.5m; they said:

We have adjusted these to reflect underspends, notified to us by the DWP, on the amounts collected under last year’s money guidance, pensions guidance and debt advice levies.

Let’s go back to that 80% increase, cited at the beginning. The 2020/21 debt advice funding pot was £63.2m – the increase to £76m in 2023/24 is 20% at best.

If we err on the side of generosity and plum for the 2019/20 figure of £53.3m then the £76m represents an increase of 42%. It’s better, but it’s a long way off 80%.

Even we go along with the £47.2m funding ‘envelope’, it’s a 60% increase. So where on earth does 80% come from?

Current funding of community advice until the end of January 2023 is £33.6m — this leaves £47.1m funding remote advice (contact centres). We can say with some confidence that the community grants for February 2023 (£30m) represent a definite 10% cut to community funding.

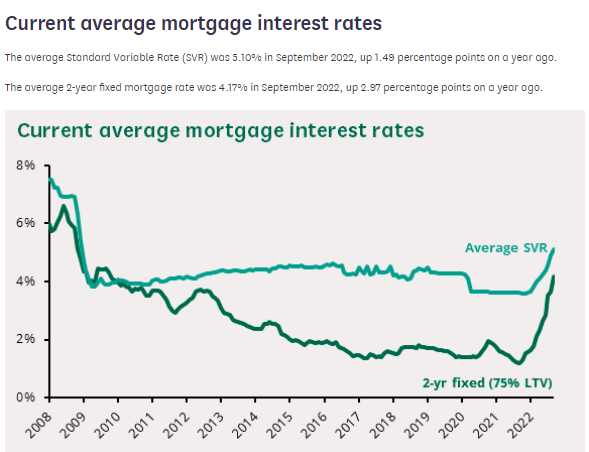

Some would argue (and I’m one of them) that the cost of living crisis, the highest rates of inflation for 40 years, personal indebtedness soaring and mortgage rates looking like this:

…require the same additional funding to debt advice that the pandemic warranted, if not more. This would help community organisations balance their own tightened budgets, recruit the staff they need to meet increased demand, continue the training of staff taken on in 2020 and, maybe, even give their existing staff a decent payrise.

***

Finally, there remains the problem of the apportionment of the budget in favour of remote advice. Mr Wyman (p19, point 33) concluded it was cheaper to give debt advice ‘online’ (£9 — per what?? Hour? Contact?), or by telephone (£70 per ??) than in person: a whopping £160 per….something. Well, of course it is! Because you are doing so much less for the people who need the help. And if each person who needed that in depth advice, comes away from these remote experiences with a 6-inch thick info-pack on every debt solution known to mankind, the risk is that the advice won’t help them at all — and we’ll never know.

Unfortunately, MaPS were convinced by the cheaper = more = value for money argument, and the debt advice ‘sector’ is infested with impressive but utterly meaningless statistics. 500 calls ‘dealt with’ is not the same as 500 people achieving a useful outcome. 500 people advised to claim a benefit is not the same as 500 people actually claiming and receiving that benefit.

I’m very wary of organisations who suggest that they ‘empower’ clients by sharing information from a website/benefit calculator/budgeting tool, when what the client needs is a expert professional to sit with them, read their letters, give them time, advise them and, yes, empower them with knowledge, and a plan. True empowerment is a thing you can witness in advice.

Professional advisers don’t foist useless in-depth advice on people who don’t need it either. We are completely able to offer light touch advice or signpost information if that’s what the client needs.

We can also do remote advice — we use telephones and webchat and video-conferencing. Some of us even use WhatsApp!

***

This whole procurement exercise has been flawed from the start. We Are Debt Advisers wanted the whole thing scrapped, with proper consultation and a better understanding by MaPS of what debt advice is before it gave £46m of precious funding to remote services, especially when one of the remote service providers is a commercial, profit-making entity with a not exactly glowing reputation. That opportunity is now gone, but it is to be hoped that MaPS’ promise to engage with frontline advisers is a sincere one, and that we can yet turn this ship around.

Visit and follow Amy’s Medium Blog for more